TL;DR

– Questions of selectivity of tax advantages increasingly raised by national authorities to deny application of such advantage

– In case at hand, selectivity of ‘intragroup restructuring’ exemption with respect to real estate transfer tax examined by German Bundesfinanzhof, which has doubts and refers the matter to the Court of Justice

Introduction

In recent years, the interpretation of the ‘selectivity’ requirement in Art. 107(1) TFEU has caused a significant amount of controversy. The primary driver of this controversy has been the European Commission, which has launched several high-profile investigations into tax regimes of, and tax rulings granted by, several Member States.

In all of these fiscal State aid investigations, the condition of selectivity is key. This is logical. As AG Kokott has argued in her opinion in Case C-66/14 (Finanzamt Linz), “[i]n matters of tax law […], the decisive criterion is whether a provision is selective, because the other conditions laid down in Article 107(1) TFEU are almost always satisfied.” (§114). Furthermore, although AG Kokott (similar to other advocates general) has warned against an overly broad interpretation of the condition of selectivity, in the light of the distribution of competences within the EU (§113), recent case law has not grasped the opportunity to impose limits on the concept of selectivity.

In light of this, taxpayers are increasingly cautious to make use of certain tax advantages offered to them by Member States. In a sense, they are “looking a gift horse in the mouth” (see L. De Broe, “The State Aid Review against Aggressive Tax Planning: ‘Always Look a Gift Horse in the Mouth”, EC Tax Review 2015, 290 et seq.). Tax administrations have also taken notice of the wide scope of the concept of selectivity, and are increasingly denying the benefits of certain (advantageous) tax provisions, on the basis that conferring such advantages would amount to a grant of State aid (see also ‘Important outcome’ infra).

A recent case before the German Bundesfinanzhof (BFH) is aligned with this trend (BFH, 30 May 2017, II R 62/14). In this case, the tax authorities denied the application of an exemption from real estate transfer tax (RETT) for transfers occurring in the context of ‘intragroup restructurings’, which is embedded in § 6a Grunderwerbsteuergesetz (GrEstG). Before the BFH, one of the parties raised the question whether the provision constituted unlawful State aid. As the BFH could not conclusively decide whether provision falls within the scope of Art. 107(1) TFEU, it made a reference for a preliminary ruling to the Court of Justice (CJ).

Facts

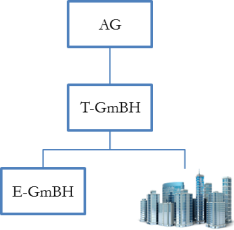

The underlying dispute before the referring court can be summarised as follows. The claimant is a German AG, which owns 100% of the shares of T-GmbH, a company owning real estate as well as shares in another company, E-GmbH.

The German tax authorities (Finanzamt) argued that the transfer of real property constituted a taxable transaction for German real estate transfer tax (RETT) purposes. The tax authorities denied the application of the exemption from RETT for transfers of real estate in the context of ‘intragroup restructurings’ (§ 6a GrEstG), which provides that transfers between controlling companies and controlled companies (i.e. companies of which at least 95% shares have been continuously held directly or indirectly by the controlling company for a period of at least 5 years before and after the transfer) are exempt from RETT.In 2012, T-GmbH was merged into AG, in the context of which T-GmbH was dissolved without being liquidated and all of its assets and liabilities were transferred to AG (incl. the real estate). At the time of the merger AG had owned (100%) of the shares of T-GmbH for a period exceeding five years. After 2012, AG has remained the sole shareholder of E-GmbH.

The taxpayer brought a claim before the Finanzgericht Nürnberg, which ruled that the RETT exemption for intragroup restructurings should be applied to the transaction at hand. The tax authorities brought an appeal before the BFH. The German Bundesministerium der Finanzen (BMF) intervened in these appeal proceedings, and flagged to the BFH that §6a GrEstG might raise State aid concerns (and should thus, presumably, not be applied in casu).

Competence of the BFH

In particular, the question was raised before the BFH whether § 6a GrEstG constitutes State aid in the sense of Art. 107(1) TFEU. This would imply that, since the proper (notification and standstill) procedure ex Art. 108(3) TFEU was not followed, it would constitute unlawful State aid.

As summarised by the BFH (§37-38), national courts are competent to assess whether a measure constitutes unlawful aid:

- In general, Art. 107 TFEU does not have direct effect, meaning that national courts do not have jurisdiction to test the compatibility of national measures with such provision. This competence belongs solely to the European Commission (EC) (Case 78/76, Steinike und Weinlig, §10).

- However, Art. 108(3) TFEU does have direct effect (Case 6/64, Costa t. E.N.E.L.), which means that the national courts are competent to examine whether the notification and standstill procedure has been properly complied with. Since such procedure only applies to measures falling within the scope of Art. 107(1) TFEU, national courts will be required to interpret this provision, which falls within their competence (Case 78/76, Steinike und Weinlig, §14).

- In case of doubt, they are obliged to make a reference for a preliminary ruling to the CJ (Case C-284/12, Deutsche Lufthansa, §44).

This is also the approach adopted by the BFH: it first gives its own view as to whether §6a GrEstG falls within Art. 107(1) TFEU (see below) and then decides to make a reference for a preliminary ruling to the CJ, given remaining interpretive difficulties as to the concept of selectivity.

Interpretation of Art. 107(1) TFEU

As per the BFH, Art. 107(1) TFEU chiefly prohibits the selective granting of aid to certain undertakings or the production of certain goods (§36).

To test whether a measure is selective, the BFH refers to the CJ’s recent case law, in which it was held that this requires an examination “whether, under a particular legal regime, a national measure is such as to favour ‘certain undertakings or the production of certain goods’ over other undertakings which, in the light of the objective pursued by that regime, are in a comparable factual and legal situation and who accordingly suffer different treatment that can, in essence, be classified as discriminatory” (e.g. Cases C-20/15 P and C-21/15 P, World Duty Free Group, §54). This requires a three-step analysis, i.e. (i) a determination of a reference system, (ii) an identification of a derogation from the reference system and (iii) if a derogation exists, an examination whether such derogation can be justified by the nature or general scheme of the reference system (BFH, §44 and 54, with references).

In the case at hand, the BFH is uncertain as to whether this ‘selectivity’ condition is met with respect to § 6a GrEstG. At the outset, the BFH notes that the advantage granted by § 6a GrEstG is at first blush not limited to certain undertakings or the production of certain goods, and applies to all domestic and foreign undertakings involved in restructurings according to the laws of the EU/EEA Member States, irrespective of the nature of their activities (§47). However, the BFH had already implicitly acknowledged that such elements are insufficient to negate selectivity (§45).

Steps 1 and 2

The BFH does not explicitly identify which tax rules constitute the reference system. Instead, it merely identifies some conditions of application of § 6a GrEstG which may be considered to exclude legally and factually comparable taxpayers from the scope thereof, and may as such be indicative of selectivity) (§48 et seq.):

- The limitation to some (e.g. mergers, demergers and contributions of assets) but not all restructuring transactions. However, the BFH also notes that the eligible restructuring transactions – unlike other restructurings – all concern a change of legal ownership (‘Rechtsträgerwechsel’) that prima facie falls within the scope of the RETT, which may be an argument to deny legal and factual comparability (§49).

- The 95% ownership condition. However, the BFH also argues that transfers of ‘qualifying’ versus ‘non-qualifying’ shareholdings is are not legally and factually comparable, as the former are prima facie subject to RETT (similar to direct transfers of real estate) but the latter are not subject to RETT at the outset (§51).

- The 5-year holding period requirement(s). Here, the BFH argues that this condition could imply a differentiation between legally and factually comparable undertakings, without offering a counter-argument (§52).

In conclusion, the BHF does not exclude that (some elements of) § 6a GrEstG would be considered to be prima facie selective.

Step 3

Subsequently, the BFH examines whether such prima facie selectivity may be justified by the nature or general scheme of the reference system. In particular, the BFH notes that the derogation may be justified, as the initial scope of application of the RETT may be drawn too broad from a legal perspective, which must subsequently be narrowed down. In this respect, the BFH – in my view rightly – argues that it should be irrelevant for the selectivity analysis whether the scope of the RETT would be defined narrowly from the outset or narrowed down by virtue of a separate (exempting) provision, such as § 6a GrEstG (§57).

In casu, the BHF argues that the conditions of application are only intended to impose a limit on the (unintended) consequences related to a broad application of RETT (§58 et seq.):

- The goal of the RETT is to levy tax on the change in legal ownership (‘Rechtsträgerwechsel’) of real estate. However, due to the 100% stake of AG in T-GmbH, the former was already considered as the ‘owner’ of real property for RETT purposes. Hence, although the merger of T-GmbH into AG constitutes a civil change of ownership of real property, it should not constitute a change in legal ownership for RETT purposes (§58-59).

- The fact that § 6a GrEstG only applies to related companies is aimed to ensure that the legal consequences of the provision only applies as intended (§60).

- The fact that the provision imposes a holding period requirement is justified by the need to prevent the benefits of § 6a GrEstG from (unintendedly) applying to restructurings of companies that have been acquired only shortly before (§61).

While the BFH concludes that there are several arguments supporting the position that § 6a GrEstG does not constitute State aid, it still has doubts in this respect. Therefore, it has made a reference for a preliminary ruling to the CJ.

Important outcome

Although it will take time before the CJ will render its verdict, the judgment is highly anticipated.

Firstly, as indicated by the BFH, it is unclear to date as to how provisions (such as § 6a GrEstG) granting tax benefits should be analysed from a State aid perspective, as such provisions only apply under certain conditions of application (and, in doing so, always exclude some taxpayers) (§46). With respect to conditions of application, the CJ has always refused to give clear statements: (i) on the one hand, the fact that only taxpayers meeting the conditions of application can benefit from the measure does not automatically make it selective (Case C-417/10, 3M Italia, §42); (ii) on the other hand, applying broad and horizontal conditions of application does not automatically imply that it is a general measure (Case C-409/00, Spain v Commission, §49). Hence, as correctly summarised by the BHF, the dividing line between ‘aid-granting’ and ‘no aid-granting’ conditions of application is unclear (§46). I hope that the CJ will provide more clarity in this regard.

Secondly, there is some debate as to whether national authorities can invoke Art. 108(3) TFEU before a national court to deny the granting of a tax advantage on the basis that it amounts to an aid (i.e. it invokes EU law as a defence in proceedings where a taxpayer / applicant challenges a decision of the (tax) authorities to deny the advantage). Since the notification and standstill obligation ex Art. 108(3) TFEU is precisely directed at Member States (incl. national authorities), one may wonder whether in such cases the national authorities aren’t (unlawfully) relying on their own miscondunct (nemo auditur propriam turpitudinem allegans), which is prohibited in other areas of EU law (cfr. R. Offermans, “Symposium on State aid”, European Taxation 2017, 153-154). Other doctrine argues that Art. 108(3) TFEU can be invoked by the national authorities (A. Metselaar, Drie rechters en één norm – Handhaving van de Europese staatssteunregels voor de Nederlandse rechter en de grenzen van de nationale procedurele autonomie, Proefschrift Universiteit Leiden, 2016, 163-164). Lacking any specific guidance from the CJ at this point in time, a referral to the CJ to this effect would be welcome. Absent such referral by the BFH, it is to be expected that this issue will remain unsettled for a while.